Professionals in any industry need to know how to reduce professional liability exposure. In particular, business owners will likely run into occasional unexpected expenses. However, business leaders can mitigate any unplanned costs with the correct insurance and coverage levels. Helping your clients get the coverage they need is one of your primary goals as an insurance producer.

Some forms of insurance are a legal requirement for doing business, while others are optional. Even optional insurance policies can be critical, depending on the circumstances. For example, while the law may not mandate carrying liability insurance, it considerably reduces risk for a business. While employees can be an organization’s most valuable asset, they can also be the greatest vulnerability. As an insurance producer, you need to explain to business owners why liability insurance is essential and the steps to reduce professional liability risk.

Why Business Owners Need to Reduce Liability Exposure

Reducing liability exposure is crucial for ensuring a business owner doesn’t get sued. A lawsuit could spell the financial ruin of a business, which is why some industries or states mandate professional liability coverage. Some companies may also want to buy professional liability insurance to cover their employees.

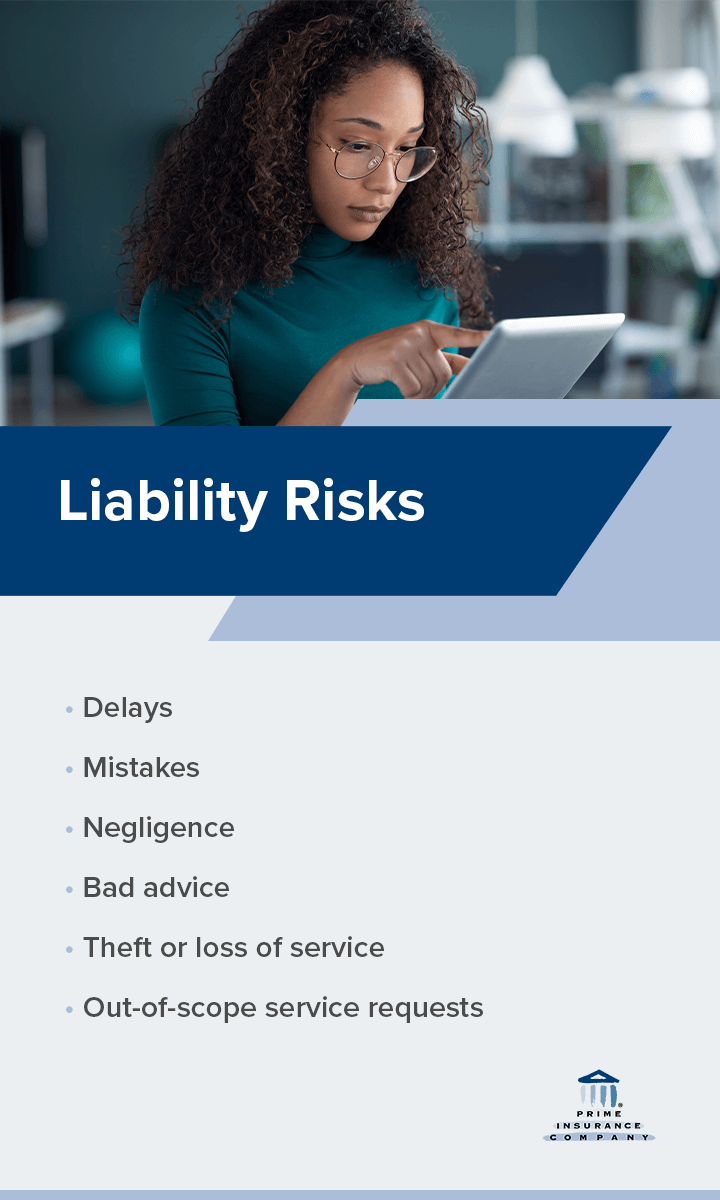

Liability Risks

Liability can arise in various ways, making it critical that businesses have the proper coverage. While your clients can always take steps to reduce their liability exposure, they likely can’t eliminate every risk.

- Delays: A business can sue another due to a delay. For instance, if a customer orders furniture from a store and the store ships the furniture, but it does not get delivered within the expected time, the customer may decide to cancel the order or ask for a refund. The store may then sue the delivery company for the loss of a customer.

- Mistakes: Every person is prone to human error, but mistakes can be expensive in many professional positions. For example, an accountant may make a miscalculation in preparing and filing a client’s tax return. A surgeon may mix up two patients’ charts and perform a gastric bypass on someone who was supposed to receive heart surgery. These errors can be costly if they result in a lawsuit.

- Negligence: Nearly any customer can sue a professional for negligence, which is the failure to do a job correctly. For example, if an accountant files a tax return that includes several mathematical errors, the tax agency may refuse to give the client a refund, and the client can sue the accountant for negligence. In this case, submitting a mistake-free tax return was the accountant’s professional duty.

- Bad advice: Giving advice that leads to a client’s monetary loss can result in a lawsuit. For example, if an investment adviser suggests their clients invest in a company that later goes bankrupt, those people may decide to sue.

- Theft or loss of service: If a business owner frequently loses things, this could cost them considerably in a professional context. For instance, if a couple hires a wedding photographer who misplaces the flash drive with the pictures before the couple receives them, they could sue the photographer for this loss.

- Out-of-scope service requests: Sometimes, clients request services outside the scope of what a provider offers. For example, a business owner may ask their accountant for business management advice, but the accountant should not make business decisions on the client’s behalf. Providing services beyond the extent of typical offerings can invite litigation.

Though a professional might face many liability risks, there are several ways to reduce liability claims.

How to Reduce Professional Liability Exposure

Every business can benefit from proactively reducing professional liability exposure. Professional liability lawsuits come at a high cost, but fortunately, various risk management tools and methods exist. The following are steps to limit liability.

1. Communicate With Clients

Improving communication with clients can prevent professional liability lawsuits. When a business owner checks in with clients, the owner will quickly know whether the clients are unsatisfied or considering going in a different direction. Ideally, clients would approach the business owner with their concerns, but it remains the owner’s responsibility to maintain an open line of communication.

2. Cut Ties With Risky Clients

One of the ways for a company to reduce liability claims is not to offer services to risky clients. For example, a CPA may want to stop serving uncooperative, argumentative clients who require constant hand-holding or frequently cause a crisis-oriented culture.

No matter the industry, the goal is to work with the best-quality clients and reduce the odds of litigation. Though it can seem counterintuitive to grow a business by severing ties with clients, some customers represent more of a threat than an asset.

3. Get Client Approval at Every Major Phase

During every milestone of a project, a business should ensure the client gives their approval and understands the progress taking place. This transparency will demonstrate to customers that they are getting what they want from the project and help prevent professional liability.

4. Provide Employees the Necessary Training

Leaders should know what they’re doing, but due to employee turnover and promotions within the organization, personnel can assume leadership positions without having the required experience or receiving the necessary training. To avoid substandard performances and work in a business setting, employees should have adequate education on their roles. Investing in training will help reduce professional liability exposure in an organization.

5. Develop a Resolution Procedure for Customer Complaints

Additionally, companies should have a process in place to resolve customer complaints. A business should implement a procedure that provides guidance on tracking and responding to concerns, including documenting the response. Written procedures can prevent minor issues from snowballing and getting out of hand. If a business faces a lawsuit, it will have a record of every step taken to resolve the customer complaint.

6. Encourage Professional Skepticism

In a business, it’s critical to strike a balance between familiarity and professional skepticism. While there’s nothing wrong with maintaining a friendly attitude with clients, staff must keep a questioning attitude in every engagement.

7. Communicate the Need for Deadline Adjustments

A company should take every step necessary to meet deadlines. However, if someone will miss the assignment’s due date, they should inform the client sooner rather than later. A delay could interrupt a client’s workflow, which can be expensive and complicate the client’s relationship with its customers.

8. Ensure Engagement Leaders Handle Quality Control

Even if another staff member has ample experience and qualifications, an engagement leader shouldn’t delegate their quality control responsibilities to anyone else. People in this role should stay continually involved to ensure tasks get completed correctly. Doing so can help mitigate liability risk and increase profitability.

9. Educate Clients About Preventing Data Breaches

Education is critical to preventing data breaches. Depending on the work a business does for a client, it may want to offer general or specialized data security training that will educate clients about how the installed technology works, what settings should be in place and how employees can best use the technology for the optimal security results. Doing so will help reduce professional liability exposure.

10. Discuss and Deliver Engagement Letters

An engagement letter is an enforceable contract that depends on each party understanding the letter’s contents. For example, during discussions with clients who are CFOs or CEOs, an engagement leader can learn information about adverse economic effects, possible fraud and changes in an organization’s operations.

By communicating this information to the proper engagement personnel, companies can increase efficiency, ensure engagement quality, eliminate the chance of lawsuits and reduce professional liability.

11. Define the Scope of Services Offered

In business, it’s always better to overcommunicate than assume everyone is on the same page. A professional who does work beyond their services’ scope could open themselves up to professional liability. Before beginning a project, providers should define its parameters and confirm the work they will perform for clients.

12. Restrict the Use of Sensitive Reports

In high-risk situations or circumstances, restricting the use of reports can limit professional liability exposure. It’s typically appropriate to do so when there is any concern about unauthorized or unqualified people using the financial statements or information. To secure financial information in a high-risk circumstance or specialized industry, a company should restrict the use of review, audit or compilation reports.

13. Structure the Business Properly

Choosing the best way to structure a business is a crucial decision for limiting the risk of liability and reducing the costs of lawsuits. For example, a limited liability corporation can protect sole-proprietorship businesses and small businesses. In the event of a lawsuit, a business owner who has chosen an LLC structure will typically not need to worry about personal assets.

Alternatively, a corporation can also provide vital protections to an organization. A business owner should determine which structure is more appropriate to get the protections needed and reduce professional liability exposure.

14. Integrate Quality Control Procedures and Policies

Engagements should integrate quality control procedures and policies intended to create high-quality engagements and limit exposure to legal liability. Documentation should include proof of how employees used quality control procedures and policies during the job. This documentation can ensure compliance with the relevant professional standards and reduce time spent on peer reviews.

15. Obtain Appropriate Insurance Coverage

A few types of available business insurance can meet various needs, including general liability insurance, home-based business insurance, product liability insurance and commercial property insurance.

- General liability insurance: This type of insurance covers incidents of general liability, such as third-party injuries, accidents and claims of negligence.

- Home-based business insurance: This type of insurance covers losses for home-based businesses that homeowners insurance will not. Though there may be riders available for some homeowners insurance policies, it might be beneficial to purchase a policy intended for home-based business coverage. If people regularly visit or work on a business’ property, this insurance provides coverage in the event of an injury.

- Product liability insurance: This type of insurance protects a business when someone sues on the basis of a defective product that led to bodily harm or injury.

- Commercial property insurance: This type of insurance covers damage and losses to a company’s physical property.

Business owners should be aware of all liability coverage options available to them to ensure adequate protection.

16. Purchase Professional Liability Insurance

Your clients may also want to consider purchasing professional liability insurance. Even the most careful, conscientious service providers make mistakes. Unfortunately, when a mistake leads to damage or an injury to someone else, the injured party is within their rights to pursue legal action that could have significant financial implications for a business or professional. At Prime Insurance Company, our professional liability coverage options include the following.

- Commercial liability: Commercial liability provides a business with general liability coverage for property damage or bodily injury sustained by a third party during the administration of services.

- Malpractice: Malpractice insurance covers omissions and errors made by a physician, nurse or another health care provider.

- Customized special liability coverage: Customized specialty liability insurance offers coverage for events or incidents that are specific to the policyholder’s occupation or business.

- Wrongful acts: Wrongful acts coverage applies to any alleged or actual breach of conduct or errors that occur while providing professional services.

- Alleged assault and battery liability: Alleged assault and battery liability provides a company with protection against assault or battery allegations.

- Alleged sexual abuse and molestation liability: Similarly, alleged sexual abuse and molestation liability insurance protects businesses against allegations of sexual misconduct made against the policyholder or a company employee.

We also offer excess coverage options, for claims that might exceed the policy limits of a standard liability policy.

Contact Prime Insurance Company About Professional Liability Insurance

At Prime, we provide professional liability coverage to professionals in various industries, including medical professionals, teachers, police officers, administrators, firefighters, midwives and volunteers. We offer customized coverage and solutions to individuals, businesses and producers when standard markets don’t meet your needs.

We treat everyone we insure as a partner by taking a hands-on approach to finding unique solutions for every client’s insurance needs. By writing policies for tough or misunderstood risks, we provide the coverage your clients need. When producers partner with us, they can grow their book of business, expand their portfolio, stop turning away specialty opportunities and earn more money.

We proudly uphold an A rating from AM Best*, and we will strive to get your clients the professional liability coverage they need. Contact us at Prime about professional liability insurance today.

For latest ratings, access www.ambest.com.

___________________________________________________________________________________________

Reviewed by Rick Lindsey, Owner of Prime Insurance

Reviewed by Rick Lindsey, Owner of Prime Insurance

Rick Lindsey hails from Salt Lake City, Utah. He began working in the mailroom of his father’s Salt Lake City insurance firm, getting his introduction to the business that became his lifelong career. Lindsey quickly rose through the ranks while working in nearly every imaginable insurance industry job. As an entrepreneur, specialty lines underwriter, claims specialist, risk manager, and a licensed surplus lines broker, Rick Lindsey is highly skilled in all levels of leadership and execution. As he progressed on his career path, Rick discovered an urgent need for insurers willing to write policies for high-risk individuals and businesses. He was frequently frustrated that he could not provide the liability protection these entities desperately needed to safeguard their assets. He also formed the belief that insurance companies acted too quickly to settle frivolous claims. Lindsey decided to try a different approach. He started an insurance company and became the newly formed entity’s CEO. This opportunity has enabled Rick to fill a void in the market and provide a valuable service to businesses, individuals, and insurance agents who write high-risk business. Prime Insurance also specializes in helping individuals and businesses who live a lifestyle or participate in activities that make them difficult for traditional carriers to insure. If you’ve been denied, non-renewed, or canceled coverage, don’t give up quite yet. Chances are Prime Insurance can help.