A New Market For Distressed Commercial Auto Risks

PPCI offers the capacity to ensure any commercial auto risk class with adverse account experiences such as unsatisfactory loss experience, poor driving records or lack of insurance history. PPCI’s partnership approach, based on customized underwriting, extraordinary claims handling and risk management, produces outstanding results for our partners. PPCI will be the difference between producers keeping clients in business as opposed to having them close their doors.

The Florida Department of Transportation reported that in 2015 the state had 19.7 million registered vehicles and 16 million licensed drivers making it one of the country’s largest commercial auto markets. Among these are many commercial auto owners, employers and operators who need to ensure their vehicles and drivers and are having tremendous difficulty obtaining insurance due to imperfect histories or atypical business arrangements. “Producers have been frustrated by their inability to meet the needs of clients and have been lobbying the Florida Office of Insurance Regulation for a market for their very hard-to-place commercial automobile business.

Types of Commercial Automobile Businesses That Need Insurance Coverage

Car Washes

Car washes get all types. A truck covered in mud could be followed up by a high-end vehicle looking for a premium wash before an event. If your clients’ employees don’t know what to do in all circumstances, you and they could be looking at a hefty claim for damages. If the car washes you cover are starting to become riskier than their last valuation, consider making these changes in the packages you offer them.

- Offer discounted premiums for proof of training

Demand changes depending on the neighborhood of the car wash. Break down your clients’ common claims or incidents based on geography and type, then consider offering discounts or other incentives for proof of training on how to clean, wax, and detail across the widest range of incidents. The money and time saved by reducing incidents are worth a smaller reduction in revenue.

- Make sure your clients’ policies include coverage for common incidents

While paying for damage or settling claims takes money away from your company, clients will get frustrated if their problems fall outside your area of coverage. Make sure the policies are tailored to the bulk of their risks.

- For high-risk clients, consider excess liability coverage

Car washes near high-end neighborhoods, expensive universities with out-of-state students, and other locations with pricey cars need more coverage. Not only will they be more likely to offer a wider range of services, owners of expensive cars are less forgiving of damage.

Going from an Automated Car Wash to a Full-Service Operation

Different car washes have different risks. A traditional, low-maintenance model where customers bring their own quarters and wash their own cars are the lowest risk of all, especially because there’s limited interaction between your client’s employees and the customers of their cars. But the risk rapidly escalates from there as car washes change to automated drive-throughs or to full-service car washes.

Which risks increase as car washes increase their services?

Liability coverage for damage to vehicles

At full-service car washes, your client’s employees are getting behind the wheel of several dozen cars a day. Not only does that exponentially increase the risk of damage to each of the vehicles being handled, it means there’s an increased risk of collision between two third-party vehicles that your client is responsible for. If your client is considering adding a full-service option, evaluate the added risk.

Equipment breakdown coverage

The lowest maintenance car washes have relatively few moving parts beyond the dispenser. But automated car washes have several automated brushes, a boiler, and more. As the operation becomes more complex and liable to break, the coverage needs to change to incorporate the higher likelihood of expensive repairs.

Going over insurance limits

Even if your client keeps you informed of ongoing transformations to their business and their overage changes accordingly, the new changes could increase incidents and claims as employees get used to the changes. If your client needs additional coverage for both during and after the transition, let them know before the next claim.

Car Dealerships

As a car dealer, you love putting customers into new or used cars at a great price. Let’s face it, there’s no greater satisfaction than closing a deal. But what about the risks of owning or running a dealership? A customer takes a car out for a test drive and hits another car. A salesman clips another car in your lot. A customer’s car is stolen while on your premises. Your inventory gets damaged during a flood or hurricane. How about a simple slip and fall on your property?

Case in point: a customer in a New York dealership sued the dealer for $50,000 when she slipped on a carpet that was drenched with water. Can you afford the financial damage of a lawsuit? How, then, do you protect yourself — and your business — from financial ruin? Specialty liability insurance from Prime Insurance Company, Inc. is your best protection against litigation. Specialty liability insurance goes well beyond general liability insurance to cover the more difficult or unusual risks that car dealerships face. Prime Insurance is a leading insurer for clients that carry unusually high risk. Prime follows a bold business model that has inspired 30 years of success and growth.

We provide fast, flexible underwriting and a partnership approach to specialty liability, professional, property and casualty insurance coverage. Our proven approach to underwriting, risk management, and claims makes Prime one of the most recognizable, memorable and preferred carriers of specialty insurance. Prime can help you rest easy with Dealers Open Lot Insurance, which covers any physical damage to your vehicles; Garage Liability for claims of bodily injury and property damage; and Garage Keepers Legal Liability, which protects your customer’s vehicle while it’s at your place of business for service.

Prime Insurance Company is driven to protect car dealerships, easily, efficiently and cost-effectively.

Dealer New Cars Stock. Colorful Brand New Compact Vehicles For Sale Awaiting on the Dealer Parking Lot. Car Market Business Concept.

Prime Company Provides Commercial Auto Coverage Across the United States

Prime Insurance Company has been approved to write commercial auto liability coverage under Prime Property and Casualty Insurance Inc. The admitted company will provide options for those who have claims, bankruptcy, substandard DOI scores and more. PPCI will help provide solutions when coverage is hard to find.

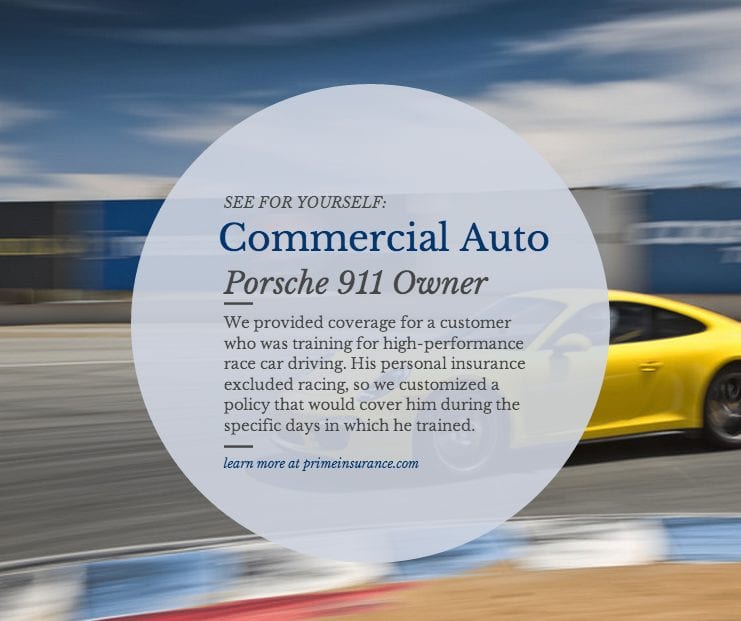

We are dedicated to insuring specialty, hard-to-place risks while providing unique solutions for risks that are denied by other markets. Many have found us to be a valuable resource for their business that cannot be found elsewhere. Our underwriting expertise lends itself the ability to underwrite specialty insurance of all kinds. Included is this unique, customized solution that we provided for hard-to-place risks in the marketplace.

Whatever the degree of risk or difficulty, we will provide customized options and deliver a quote on the risk.

Last updated 15 October 2021

___________________________________________________________________________________________

Authored by Rick J. Lindsey, CEO, President, and Chairman of Prime Insurance Company

Authored by Rick J. Lindsey, CEO, President, and Chairman of Prime Insurance Company

Rick J. Lindsey hails from Salt Lake City, Utah. He began working in the mailroom of his father’s Salt Lake City insurance firm, getting his introduction to the business that became his lifelong career. Lindsey quickly rose through the ranks while working in nearly every imaginable insurance industry job. As an entrepreneur, specialty lines underwriter, claims specialist, risk manager, and a licensed surplus lines broker, Rick Lindsey is highly skilled in all levels of leadership and execution. As he progressed on his career path, Rick discovered an urgent need for insurers willing to write policies for high-risk individuals and businesses. He was frequently frustrated that he could not provide the liability protection these entities desperately needed to safeguard their assets. He also formed the belief that insurance companies acted too quickly to settle frivolous claims. Lindsey decided to try a different approach. He started an insurance company and became the newly formed entity’s CEO. This opportunity has enabled Rick to fill a void in the market and provide a valuable service to businesses, individuals, and insurance agents who write high-risk business. Prime Insurance also specializes in helping individuals and businesses who live a lifestyle or participate in activities that make them difficult for traditional carriers to insure. If you’ve been denied, non-renewed, or canceled coverage, don’t give up quite yet. Chances are Prime Insurance can help.